The Financial Seminary

7403 Divot Loop

Bradenton, FL 34202

ph: 941-544-5976

garmoco

- Home

- The Omega Series

- Guest Articles

- In The News

- Articles

- Ayn Rand & Donald Trump

- Losing Faith

- Does Our House Divided Need...

- Reaganomics

- Pursuing Ponzi Protection

- Does God Want You to Be Rich?

- Responsible Capitalism

- Introducing Stewardism

- Thanksgiving Sermon 2011

- The 9.5* Theses of Stewardship

- Charity in Truth

- Blessed to be a Blessing

- The People vs The Prophets

- Email to Christianity Today

- Holiday Meditation

- Resources

- On Ayn Rand

- Videos

- POWERPOINTS

- About Us

- Contact Us

- Archive

Class Fifteen

"Any fool can make things bigger, more complex and more violent.

It takes a touch of genius--and a lot of courage--to move in the opposite direction."

Albert Einstein

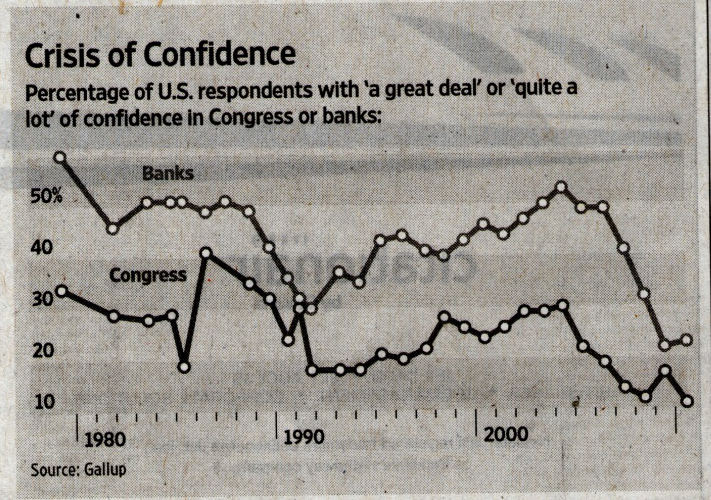

Source: Wall Street Journal, February 9, 2011

I'm angry, to the point of imitating that guy in the movie who famously screamed: "I'm mad as hell and I'm not going to take it anymore." While most Americans seem to be mad at big government, I'm angry at another BIG, Bankers Ignoring Guidelines of human decency. After all, this old political science graduate understands that every politician in Washington has been elected by a majority of Americans who bothered to vote somewhere. If we're angry, we can only be angry with ourselves. But I don't know of any CEO of any big bank who's been chosen by anyone outside the bank's boardroom. And John Bogle, who founded the Vanguard Mutual Funds before retiring to focus on the ethics of managing our nation's money, recently chose to begin his book Enough with these words: “The people who created this country built a moral structure around money. Over the past thirty years much of that has been shredded. The country's moral guardians are forever looking out for decadence out of Hollywood and reality TV. But the most rampant decadence today is financial decadence, the trampling of decent norms about how to use and harness money."

Winston Churchill once said a man is only as big as the things that make him angry. Churchill was angry at Hitler. But like another fellow who was slow to anger but big on principle once there, I'm ready to whip some money-changers in the temples of American capitalism, our banks. I have no delusions that I will have any more effect than that angry fellow did two thousand years ago. But sooner or later, if a man grows big enough, he has to take a stand for what he loves. And I still love America as it was when banks were smaller. Others must as well. It takes very hard work to inspire only slightly more confidence in Americans than does Congress! That's a very big deal. The article around the chart above described the very clear ties between our lack of confidence in banks and our housing mess, elevated joblessness and anemic recovery. That pains this old guy who entered financial services during the late seventies when ours was still a generally respected industry.

Over four decades ago, I left my small town where everyone knew my name. It was the kind of town where, for example, when this college freshman ran out of money in his checking account, a bank officer would call my parents so one of them would stop by in the next few days to transfer enough to cover my deficit. We didn't have ATM's, or need them as we had time to talk to our neighbors at the bank; but the bank wouldn't have thought of bouncing one of my checks as my parents and the people in the bank had decades of relationship.

But perhaps foolishly, this small town guy attended a big university in order to study the governance of our big country. I was a conservative who believed government was best when it's small and close to home. I still expect the Tea Party will be a good thing, even if I hate the spiritually impoverishing paranoia and financial hoarding produced by their political propaganda. I therefore expect the Union will survive. But since our big financial institutions and big government played a dominant role in ushering in the Great Recession with irresponsible mortgage lending, I've increasingly had a different concern. I'm now convinced that business, and banking in particular, is also best when it's small and close to home.

I began to wonder about how we conservatives often hate big government but love big business when I was in management training with a big Wall Street firm. As we weren't Goldman Sachs, most of us were conservative. But we never gave a thought to the fortunes we were making underwriting and trading more and more government-guaranteed debt. Nor did we ever wonder if investment banking might be better if our firm was smaller. Everyone simply seemed interested in making ever bigger money by doing bigger and bigger deals. But big institutions prompted the Crash of '87 and my firm sought to throw me over-board with other management trainees it no longer needed. I became an independent advisor.

But I was recently reminded of the old saying growth for its own sake is the philosophy of the cancer cell. My son Garrett recently got engaged and wanted to buy an inexpensive condo as it was a third of its price of a few years ago and the payments were smaller than renting. He had earned a salary working with us the previous two years. But I assumed that would be insufficient for him to get a mortgage while our banks are obsessed with recapitalizing their own finances after years of reckless lending. So I went to my branch of Bank of America to borrow a relatively small amount against our home so I could finance Garrett's new home. We had paid off a couple of BofA mortgages in the twenty years we'd banked there and had an unused home equity line. So I didn't anticipate any difficulties. Unfortunately, my local contact, who is a devout Christian for whom I've spoken gratis at her church, only takes in money. You have to talk to an unfamiliar--and far less friendly--face if you want to get any of it back in the form of a mortgage loan.

So my friend at my branch gave me the card of BofA's mortgage salesman who operates in the community up the road. This most abbreviated version of our experience should be clearly understood by any young person aspiring to home ownership; any person hoping to manage or work for a small business like ours; any politician who's wondering how to jump-start the housing market on which our economy and jobs so depend; and any shareholder who wonders why Warren Buffett recently sold his BofA stock even though BofA's president has gone high profile in promising a "new era" of greatly improved earnings despite our government threatening it with fines in the billions for incompetent mortgage foreclosures.

For reasons completely unknown to me, when I first telephoned the mortgage salesman and discussed my situation, he assured me that Garrett could qualify for his own mortgage through FHA. He could "lock-in" a 4.25% fixed-rate, thirty-year mortgage. So as I've encouraged Garrett to faithfully pay off borrowings to establish sound credit, that sounded like a good idea...at the time. After six months of what I can only describe as swimming in a financial hell fire and brimstone, and after talking to several people who described similar treatment from BofA's mortgage unit, I now very seriously refer to BofA as SofA, or the Scandal of America. My experiences, and those of friends, suggest SofA's mortgage unit is simply the most inefficient and ethically-challenged financial enterprise I've had the displeasure of encountering during thirty years on Wall Street. And that's saying a lot. Worse, it was Garrett's introduction to the real world, rather than academic world, of big money. He's now wondering if he wants to dive in after all. He certainly won't want to market any of the SofA bonds our firm's bond department has in inventory or any SofA mutual funds. Whether he'll ever trust another bank is doubtful. He has very good reason.

After six months of rising mortgage rates complete with oral and written promises that Garrett was protected, SofA rejected his loan. The rejection came the very same day that he was to fill out new paperwork they had sent and SofA conducted an appraisal. That indicated the crazies in SofA's mortgage asylum don't even talk to each other, much less clients. Their official reason for rejecting the loan? Our unincorporated small business has paid Garrett with our personal checks rather than corporate checks so his income supposedly "does not meet FHA guidelines for income verifiability." Yet their report from the IRS showed Garrett had paid taxes on that money and three credit rating agencies gave him scores of around 750. When I complained to my friend in my local branch, and to two other FHA lenders since, I was assured the kind of checks his salary was written on had no bearing on FHA loans. I don't know but I expect the other bankers are correct that SofA simply didn't want to give Garrett the rate he had "locked-in." Otherwise, you'd have to believe SofA is worried we simply gave Garrett, and the IRS, all that money over the past two and a half years just so he could get a mortgage he didn't know he wanted until SofA sold him on the idea six months ago. Even they can' t be that crazy.

The truly scandalous thing about our experience however wasn't SofA's unbelievable incompetence but its even greater arrogance. It was virtually impossible to get anyone to return a phone call or email. The person who knew us was in one location, the mortgage salesman was in another, his supervisor was in another and the processors were a hundred miles away. Of course, if we did manage to communicate with one of them, they simply informed us it wasn't their responsibility. I still have absolutely no idea who was in charge of my son's application. But when I finally expressed an appropriate level of indignation at how we had been treated for six months after earning almost nothing on our fairly substantial deposits year after year, I got a lecture in civility from someone half my age. Only one person seemed to know the word "sorry" and he proved irrelevant to the process.

When we finally got to talk to the salesman after the processing department had left our application lying around unattended until the rate "lock-in" was expiring, he said our processor had suffered a nervous breakdown. I sympathized as she surely worked in a boiler room operation. What I couldn't understand was management's seeming disinterest in getting her work done while interest rates were rising sharply, which continued until the second lock-in was expiring. All the salesman could say was that our experience was nothing compared to what he saw each day. He attempted a less than sensitive effort to make us feel better by literally explaining he had clients with millions in SofA who could not get a mortgage of a couple hundred thousand dollars. That certainly made me feel more confident that SofA would be there if I ever decide to ignore its counsel and apply for a loan myself!

Now let me share the shard of brimstone that seared to the depths of my soul. The very week all this was coming to a sad ending, the mortgage manager ran a flashy ad in a glitzy local magazine. The headline was: "Experience the level of service you deserve. First class." Of course, he didn't respond when I asked about the horrors of being a second class citizen in SofA hell. But the one time I did get to chat with him, he reassured me that he attends the local church of the affluent and powerful. He didn't know that meant absolutely nothing to me as I had served on a church board with Ken Lay who ran Enron, a very big but ethically-challenged financial enterprise. SofA is far more important to the America our grand-children will inherit than was Enron. And Enron was widely admired before it destroyed enormous trust in capitalism. So the really big question is what can any of us do other than provide an email lashing to the inboxes of low-level SofA employees? A couple of small things might actually be genius in their simplicity.

Only last week I received an email forwarded by a friend who is a very conservative retired businessman. Even he was angry at big oil for gouging us due to the unrest in North Africa. The email explained big oil thinks they have us over a barrel as we must have gas. But the originator of the email campaign knew better. He suggested we simply buy our gas from companies other than Exxon Mobil, the biggest of big oil. It would then have to reconsider how it's treating customers and lower its prices. As it does, other big oil companies would have to reconsider as well.That simple but shrewd idea of cutting the very biggest down to size might work with banking as well. All we have to do is stop doing business with SofA by moving our money to a community bank or credit union. SofA would grow more customer oriented or die. The prospect of death has always been the finest organizer of priorities. So SofA might again begin acting like the Bank of America rather than yet another corporation whose only concern is for corporate management.

God knows, like the other big companies in the S&P 500, SofA sure doesn't seem to have been focused on its employees, clients or shareholders the past decade. Only days after SofA rejected my son's application to finance his first home, with my deposit in a very real way, a headline in the March 11th edition of The Financial Times read: "BofA under fire over staff home-loss subsidies." The story told how stridently its management was fighting the SEC even allowing shareholders to vote on it protecting its management from losses on their own homes. And this while it was also under fire for improperly foreclosing on the homes of our young men and women fighting overseas. Apparently, there simply is no moral compass, or shame, at SofA any more.

So if you're as angry at Bankers Ignoring Guidelines of human decency as the Tea Party is at Congress, perhaps you too would also like to network. Just send us an email through our website www.financialseminary.org. For the time being, simply share how SofA's mortgage unit's hellish service bears little resemblance to its heavenly advertising. Assuming our computers don't crash and burn from all the heated emails, we might broaden our movement to Businesses Ignoring Guidelines of human decency. Who knows, this old technophobe might even help his son launch a Facebook campaign to challenge the less-than-democratically elected and supervised CEO's (Ayatollah's?) running too many of our big banks and businesses. Of course, there are a few we might want our grandchildren to emulate in later business life. But try to name three off the top of your head. Sad isn't it? No wonder so very many of our kids have to emulate athletes or entertainers. That can't bode well for our future either.

After three decades on Wall Street, I'm not so naive as to expect to irritate any CEO's. They'll likely continue to sit high atop big buildings plotting ever bigger profits from laying off ever bigger numbers of employees and asking ever bigger things of those who remain. Once shareholders awaken to the fact that CEO's can cut their way to short-term profits but not long-term growth, the CEO's will float back to earth on golden parachutes. But a slap on the back of the hand with a Golden Ruler just might get the attention of those juveniles tinkering with our engines of capitalism. It might even give them a taste of America's new hell on earth: making their incomes un-verifiable.

****

Gary Moore is a Sarasota-based investment counselor who has authored five books on the morality of political-economy and personal finance. He is a representative of, and securities offered through, National Planning Corp (NPC), member FINRA/SIPC, but opinions expressed here are his alone. The Financial Seminary and NPC are separate and unrelated. His comments are included in the More Good $ense newsletter in an effort to expand stewardship leaders’ understanding of broader economic issues.

Gary Moore is an investment counselor affiliated with NPC Of America, member FINRA/SIPC. The views expressed are his alone.

All information herein has been prepared solely for informational purposes, and it is not an offer to buy or sell, or a solicitation of an offer to buy or sell any security or instrument or to participate in any particular trading strategy.

Securities licensed associates of Gary Moore & Co., are Registered Representatives & Investment Adviser Representatives offering securities and investment advisory services through NATIONAL PLANNING CORP. (NPC), NPC of America in FL & NY, Member FINRA/SIPC, and a Registered Investment Adviser. Registered Representatives of NPC may transact securities business in a particular state only if first registered, excluded, or exempted from Broker-Dealer, agent or Adviser Representative requirements. In addition, follow-up conversations or meetings with individuals in a particular state that involve either the effecting or attempting to effect transactions in securities, or the rendering of personalized investment advice for compensation, will not be made absent compliance with state Broker-Dealer, agent or Investment Adviser Representative registration requirements, or an applicable exemption or exclusion. The Financial Seminary, Gary Moore & Co., and NPC are separate and unrelated companies.

7403 Divot Loop

Bradenton, FL 34202

ph: 941-544-5976

garmoco